A man walks past the U.S. Federal Reserve in Washington, D.C., the United States, March 16, 2022. (Photo by Ting Shen/Xinhua)

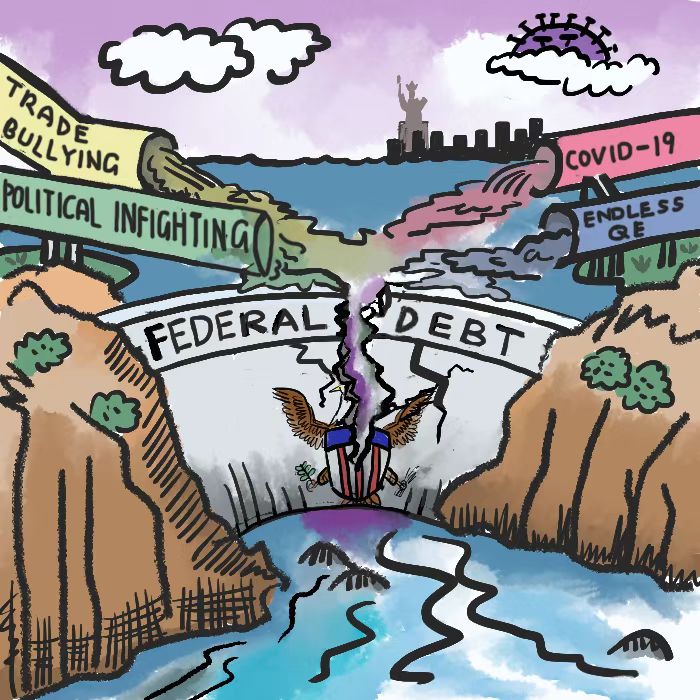

The swelling national debt number, edging closer to the 31.4-trillion-dollar statutory ceiling the U.S. Congress placed on the government's borrowing ability, has raised concerns about U.S. fiscal sustainability and its negative spillover effects on global financial markets.

by Xinhua writer Guo Yage

BEIJING, Oct. 11 (Xinhua) -- More than 33 years ago, a billboard-sized running total display was installed a block away from Times Square in New York City to remind passersby how much money the U.S. federal government has borrowed from the public and has yet to pay back.

However, this tally, well-known as the National Debt Clock, did not seem to bother successive U.S. governments, including the current administration. It read 31.1 trillion U.S. dollars for the first time on Oct. 3, and is still ticking away madly.

The swelling national debt number, edging closer to the 31.4-trillion-dollar statutory ceiling the U.S. Congress placed on the government's borrowing ability, has raised concerns about U.S. fiscal sustainability and its negative spillover effects on global financial markets.

A woman walks on the street after shopping at a supermarket in Washington, D.C., the United States, on June 14, 2022. (Photo by Ting Shen/Xinhua)

DISGRACEFUL RECORD

The total public debt outstanding reached 31.1 trillion dollars on Oct. 3, including 24.3 trillion dollars in debt held by the public and 6.8 trillion in intergovernmental holdings, said the U.S. Treasury Department's daily treasury statement released on Oct. 4.

In fact, real-time data released by the official website of the National Debt Clock showed that the debt number, having so far well surpassed 31.1 trillion, amounts to more than 93,400 dollars of debt per American citizen, and nearly 250,000 dollars of debt per taxpayer.

Given the new record, the ratio of the U.S. federal debt to the GDP has risen to roughly 126 percent, the data showed.

An estimate by British financial media outlet Finbold showed that in 2022 alone, the U.S. national debt grows by almost 6 billion dollars every day.

The number is more than the value of the economies of China, Japan, Germany and Britain combined, the Peter G. Peterson Foundation (PGPF) noted in an article published last week.

If every U.S. household paid 1,000 dollars a month, it would still take 19 years for the debt to be paid off, noted the article.

"This is a new record no one should be proud of," said Maya MacGuineas, president of budget watch group the Committee for a Responsible Federal Budget.

About eight months ago, the total U.S. public debt outstanding exceeded 30 trillion dollars, hitting a fiscal milestone. In an attempt to avert a looming debt default, the U.S. Congress passed legislation in December to raise the debt limit to the current 31.4 trillion dollars. The hike, however, failed to stop the U.S. national debt from reaching nosebleed levels.

"While much of that new borrowing was necessary to combat COVID, we are now past the most severe challenges of the pandemic, and it is time to budget responsibly -- yet we are still borrowing," MacGuineas said.

DEBT ADDICT

"The coronavirus pandemic rapidly accelerated our fiscal challenges, but we were already on an unsustainable path, with structural drivers that existed long before the pandemic," the PGPF said.

As the foundation noted, the United States has enjoyed a borrowing binge over the past decades, with its gross debt increasing from 3.2 trillion dollars in 1990 to 5.62 trillion in 2000, and then to 13.56 trillion in 2010. The country's gross debt hit 27.72 trillion dollars in 2020, and surpassed 30 trillion dollars in late January.

A significant share of the overall federal spending went to the U.S. national defense budget. An article released by the PGPF in early May showed the U.S. defense spending accounted for more than 10 percent of all federal spending, and has remained No. 1 in the world for years.

Up to Us, a U.S. non-profit aimed at creating national debt awareness on college campuses, noted in an article published in 2020 that the country's national debt hit the 1 trillion mark for the first time in history by 1982 after the Vietnam War and the Cold War.

"By the 21st century, the national debt got to 20 trillion dollars after major events such as the War on Terror," it said.

Adding to the federal government's big spending on endless wars are its massive stimulus packages, rounds of tax cuts as well as the U.S. Federal Reserve's sudden reversal of its monetary strategy from a years-long "quantitative easing" policy to a tighter one, which, noted the U.S. Bank National Association in an article in late September, "will likely result in weakening the job market as businesses slow activity in the wake of higher borrowing costs."

In December 2020, then U.S. President Donald Trump signed off a 2.3-trillion-dollar spending package. In 2022 alone, the U.S. Congress and President Joe Biden have approved a combined 1.9 trillion dollars in new borrowing, and Biden has approved 4.9 trillion dollars in new deficits since taking office.

To prevent the government from defaulting on its legal obligations, the U.S. Congress has acted 78 separate times to permanently raise, temporarily extend, or revise the definition of the debt limit ever since 1960, noted the Treasury Department.

"We are addicted to debt," said MacGuineas, adding that for decades, U.S. lawmakers have chosen to "pass politically easy policies" rather than face the challenges of true governing.

"Basically, Washington has engaged in a long-term debt spree," said a New York Times article published on Oct. 4.

Photo taken on Aug. 4, 2022 shows the White House and a stop sign in Washington, D.C., the United States. (Xinhua/Liu Jie)

TIME BOMB

"If we don't cut spending, disaster WILL come," American TV reporter John Stossel tweeted two days after the U.S. national debt reached the new record. Just as he wrote, the galloping U.S. borrowing, if not properly managed, would be nightmares for both the United States and the larger world.

As it stands, the United States is set to breach the 50-trillion-dollar mark in debt by 2030, Forbes estimated in September 2020.

In a report released in May, the Congressional Budget Office (CBO) warned that such a debt path would push up borrowing costs for the private sector, which would result in lower business investment and slow the growth of economic output over time.

To make things worse, as the Fed is determined to keep hiking interest rates to tame inflation, the U.S. government will have to pay more for its huge borrowing. The PGPF noted in an article published in September that "interest payments would total around 66 trillion dollars over the next 30 years and would take up nearly 40 percent of all federal revenues by 2052. Interest costs would also become the largest 'program' over the next few decades."

"Interest on the national debt is exploding and heading toward what economists refer to as a 'doom loop' -- the vicious circle in which the government's borrowing to pay interests generates yet more interest and yet more borrowing," a Wall Street Journal opinion noted in late September.

"The risk would rise of investors' losing confidence in the U.S. government's ability to service and repay its debt, causing interest rates to increase abruptly and inflation to spiral upward, or other disruptions," the CBO said in May, warning of the likelihood of a fiscal crisis in the United States.

Meanwhile, if the U.S. government defaults on its bills and shuts down amid bitter partisan wrangles, it would "detonate a bomb in the middle of the global financial system," Jacob Kirkegaard, a senior fellow with the Peterson Institute for International Economics, told the Voice of America (VOA) last year.

The VOA article went on to elaborate that a U.S. debt default would echo through the global economy by reducing global trade, make dollarized economies suffer, affect business contracts, erode the dollar's global reserve currency status, among others.

Back in 2011, the U.S. debt-ceiling crisis sparked the most volatile week for financial markets since 2008, with the stock market trending significantly downward. It also resulted in the country's first credit downgrade in history. Last year, when the government risked defaulting on debt again, Moody's Analytics estimated that stock prices would likely plunge 33 percent, setting off a downturn that would rival the Great Recession.

A U.S. default on its financial obligations "would very likely lead to a global financial meltdown," said an editorial published Sunday by Missouri-based newspaper St. Louis Post-Dispatch. "Even talking about that is the height of political irresponsibility." Enditem

(Xinhua reporters Xiong Maoling in Washington, and Su Liang, Deng Qian and Fu Yunwei in Beijing also contributed to the story.)■